In a previous blog I gave an example of an “ideal” wealth distribution whereby all household wealth is accumulated over the life-cycle. Even if everyone by age group has the same wealth, there continues to be age based inequality. However, by transferring some wealth to the young it is possible to reduce this aspect of inequality.

In many societies, particularly in the past, wealth transfers to the young are normal as they set out in life. In the past, when wedding parties were not as expensive as now, gifts were given to help a couple set up in their new home. Dowries are one (fairly sexist) example of wealth transfers to the young, and in some European societies the norm was for the groom’s family to give the couple land and a house, while the bride’s provided what went in the house, and the animals. These cultural norms certainly make sense where there are no financial markets where a couple can take out a mortgage to buy a farm.

Today, transfers continue to exist, especially in the form of education. Though not free, Irish education is subsidised by the state, and Irish students typically do not end up with the levels of debt that young graduates start out with in the United States. (The new wealth data can allow us to check this for certain.)

An alternative “ideal”

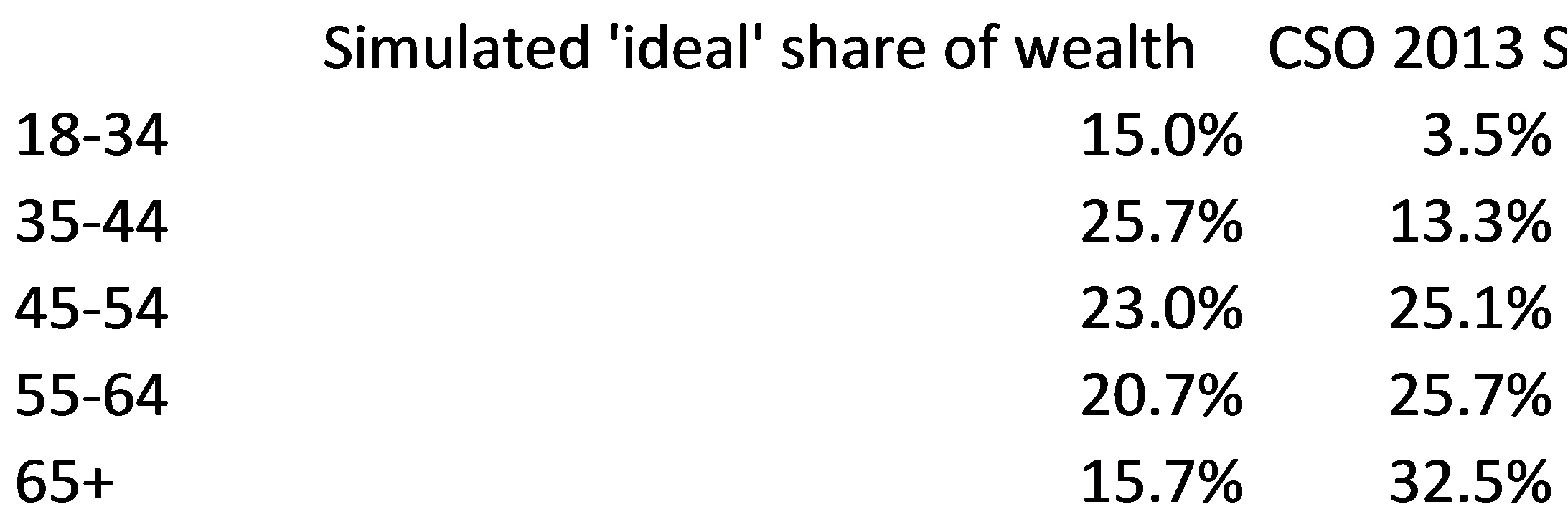

So, building on the “ideal” example of the previous post, suppose instead that the young are given a transfer of 100 units when they are 22. They save and draw down on their savings in the same pattern as the previous blog. The 100 unit gift is funded by a wealth tax at almost 4%, very close to the rate of return on investment. (An excel sheet outlining this is here.) A wealth tax close to the rate of return can be justified as fair if you think people should only earn an income from their wealth if they do something to make it increase faster than average.

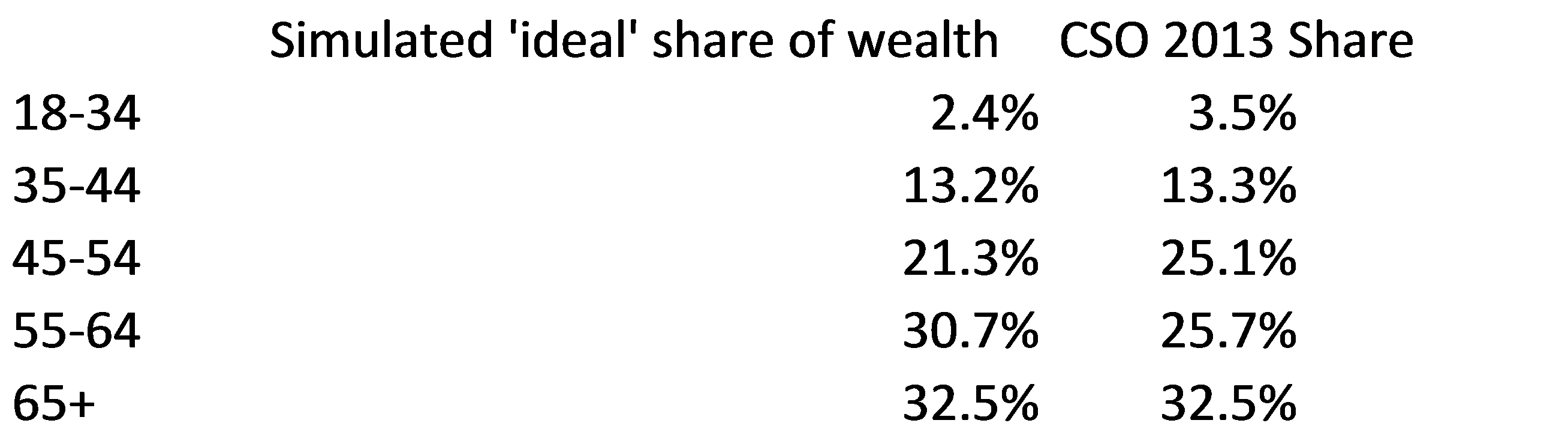

In the scenario of the previous blog the “ideal” was close to reality in terms of inequality by age (though reality has large inequality within age groups). In the scenario with transfers and a wealth tax the distribution by age is far more equal.

Wealth inequality by age does not disappear, but is greatly reduced, and the old still draw down the same amount each year as the in the earlier “ideal”. The bottom 20% of society here get almost 13% of household wealth, versus almost zero in reality, and the 17% considered “ideal” in a survey.

Is this fair

Studying economics does not give much insight as to what is fair. Other subjects such as philosophy are better at that.

A more equal wealth distribution may be wanted on fairness grounds. It can be argued that the increase in house prices since the early 1990s was a transfer from the young to the old. However, the old saved during a period when incomes were far lower.

Giving wealth to the young may also help young entrepreneurs have the finance to help them start a business.

Household wealth and the government sector

As mentioned in the previous blog, even in a communist society there would be wealth inequality by age. This is as public assets and liabilities (such as state companies, infrastructure, and the national debt) are not part of “household” wealth, but part of the state sector. This is despite the fact that citizens have a claim and responsibility for such assets and liabilities.

This can be highlighted in the above example. Is giving 100 units, and expecting the beneficiary to pay this back through a wealth tax different to a loan from a bank? Perhaps, having the wealth to buy a house as ones own early in life gives people a greater sense of security. But the two have a hugely different impact on wealth inequality statistics depsite no impact on income flows.

Measures of household wealth are just that. They are not measures of inequality in society. The complexity of society can never be distilled into a single number.

More work is needed

The above example is fairly simplistic, and definitely needs some smoothing off of edges.

No account is made for how people’s behaviour may change. Young people also save for precautionary motives rather than for life-cycle motives because credit markets are imperfect. “Human” capital can be viewed as a form of wealth, but this is not captured in household surveys. A proper analysis would make use of the available microdata, and perhaps make use of a model that shows how behaviour changes over the life-cycle. Such models exist (but to the best of my knowledge have not been used to construct an “ideal” wealth distribution).

However we definitely live in an unequal society, and this can be improved upon. It’s a matter of choice whether we want this or not.